LinkedIn vs Instagram for Fintech Marketing, What Actually Works Better?

Fintech marketing is not the same as D2C or lifestyle marketing. You’re not convincing someone to try a new snack or skincare product. You’re asking them to trust you with their salary, savings, credit score, identity and long-term money decisions.

Co-founder @anchors ; Disrupting a $23 billion Industry | NIFT New Delhi

TL;DR:

For fintech brands choosing between LinkedIn and Instagram. Focus on trust, intent, and user quality.

- LinkedIn users already think about salary, banking, investing, and financial stability

- Instagram has large reach but mixed intent and low financial decision readiness

- Complex fintech products need depth, which LinkedIn content supports better

- Higher LinkedIn costs bring better activation, retention, and user quality

- LinkedIn offers safer education, clearer data, and stronger conversion mindset

Because of this, choosing the right platform becomes more important than choosing the right creator.

Most fintech teams are torn between LinkedIn (credibility > speed) and Instagram (reach > depth).

So which one actually works better?

Let’s break it down without bias or buzzwords.

1. Audience: Who Actually Lives on Each Platform?

People open LinkedIn to think about career, salary, growth and money.

They are:

- working professionals

- managers

- engineers

- finance folks

- founders

- high-intent earners

These users already think about:

- investing

- credit cards

- banking tools

- tax planning

- financial stability

This is fintech’s core audience.

People open Instagram for:

- entertainment

- lifestyle

- visual content

- scrolling without purpose

It has a huge reach but a very mixed intent.

You may reach people who:

- are students

- have low income

- are not financially active

- aren’t in a career mindset

Instagram works well for D2C, not for financial decisions that need clarity.

2. Trust Factor (Critical for Fintech)

Financial products depend completely on trust.

LinkedIn > Trust Platform

Creators here:

- share long-form insights

- explain complex topics

- talk about credit, tax, investing

- build professional credibility

A recommendation from a LinkedIn creator feels like advice, not marketing.

Instagram > Entertainment Platform

Even if the creator is credible, the platform context makes it look like content > credibility.

Reels don’t allow depth.

Financial decisions need depth.

3. Understanding Complex Products

Fintech products need explanation:

- interest

- cashback logic

- credit score impact

- loan terms

- risk

- fees

- compliance

- limits

- insurance clauses

LinkedIn creators break these down with clarity. Instagram doesn’t support this style well.

On LinkedIn, complexity = engagement.

On Instagram, complexity = drop-off.

4. Cost of Acquisition

Fintech marketers care about:

- CPA (Cost per activated user)

- LTV (Lifetime value)

- Retention

- Deposit rates

- Credit utilisation quality

Higher CPC → but much better quality.

Users sign up, activate, and stay.

Lower CPC → but inconsistent quality.

Users often sign up casually and drop off.

"Cheap leads are expensive."

Fintech learns this the hard way.

5. Risk of Wrong Education or Miscommunication

Instagram creators often oversimplify finance to fit reels.

This is dangerous for fintech.

One wrong explanation can cause:

- compliance issues

- user confusion

- brand distrust

- financial misalignment

LinkedIn creators naturally use:

- step-by-step logic

- frameworks

- explanations

- clarity

This is safer for regulated industries.

6. Data Transparency: A Hidden Problem

A major challenge in fintech marketing is verifying creator performance.

Instagram → depends heavily on screenshots

And as you know:

- screenshots can be edited

- analytics can be inflated

- manual reporting can be manipulated

Fintech brands cannot afford this.

LinkedIn → better visibility

Creators can share verified data more easily.

In tools like anchors, data comes directly from LinkedIn, not from creators typing numbers manually.

This matters because fintech decisions rely on precision.

7. Conversion Mindset

People go to Instagram to escape.

People go to LinkedIn to improve.

Fintech conversions come from the second mindset.

This is why posts like:

- “How to improve your credit score”

- “Which bank account is best for salary?”

- “3 mistakes I made when investing”

perform better on LinkedIn.

Users save, share, comment, click — because the mindset aligns.

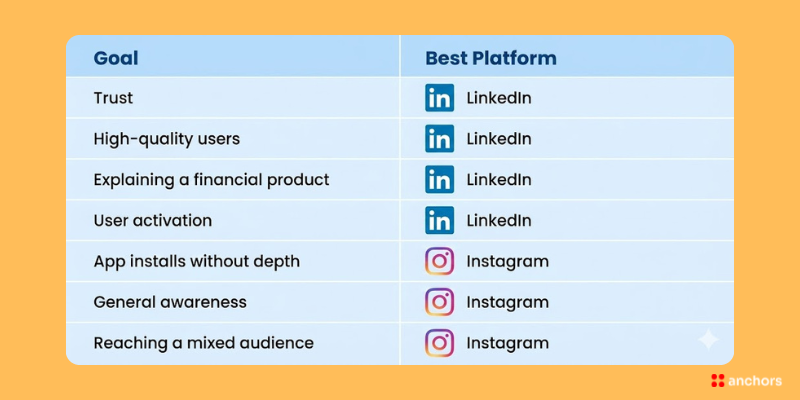

So… What Actually Works Better for Fintech?

If your goal is:

Where Should Fintech Brands Invest in 2026?

Not on the loudest platform.

In the platform that offers:

- credibility

- working professionals

- mindset alignment

- transparent data

- better user quality

- better retention

- lower long-term CAC

That platform is LinkedIn.

But the strategy needs to be thoughtful — creator selection, storytelling, clarity, and verified analytics matter much more for fintech than other industries.

Whether you’re promoting a savings feature, a credit product, a neobank, or an investment tool, the right creators on LinkedIn can influence educated decision-making.

Madhav Pangarkar

Financial & Tax Advisor to MSMEs and CEOs | Turn Tax Leaks...

CA Piyali Parashari

Founder @ Investment Beta | Chartered Accountant

Shivani Gera

Building Financial Literacy in India & Beyond | YP at SEBI |...

Palak Jain (financewithpalak)

SEBI REGD RESEARCH ANALYST | MBA FINANCE | NISM 15 CERTIFIED |...

Tushar Jejani

Management Consultant | MBA, IIML & CBS | CFA L2c | Founder,...

Explore More Articles

Discover our latest insights on SEO, content marketing, and digital strategy. Explore our curated collection of articles to enhance your digital presence.

← Scroll to explore more →